Incoterms® are internationally recognized contractual clauses which aim to uniquely identify the division of responsibilities and costs associated with transport between seller and buyer.

Although Incoterms relate to the costs and risks of transport, they must be inserted and accepted by the parties as part of the contract for the sale of goods and not in contracts for transport, shipping, insurance or financing.

The latter must subsequently be stipulated, by the party who holds the responsibility, in accordance with the Incoterms provided for in the original sales contract.

What are Incoterms and what are they for?

Incoterms® is the contraction of International Commercial Terms.

They were first created in 1936 by the ICC International Chamber of Commerce, which was born a few years earlier with the aim of facilitating international trade following the first postwar period.

The great variety of contractual terms existing at international level, to which a multitude of different interpretations were added, required a work of harmonization and identification of shared rules with the aim of reducing the risk of disputes and facilitating exchanges between different countries.

Over the years, the increase in the countries included in the analysis, the diversification of transport modes, the proliferation of container traffic and the need to simplify or clarify certain terms have made it necessary to continuously update and review the Incoterms by of the International Chamber of Commerce.

The eighth revision gave rise to the Incoterms® 2020, which were published on 10 September 2019 and which entered into force on 1 January 2020.

It is good to remember that the use of Incoterms is optional and that the previous editions remain valid and applicable, as long as they are explicitly referred to in the sales contract.

What are the Incoterms and how are they divided?

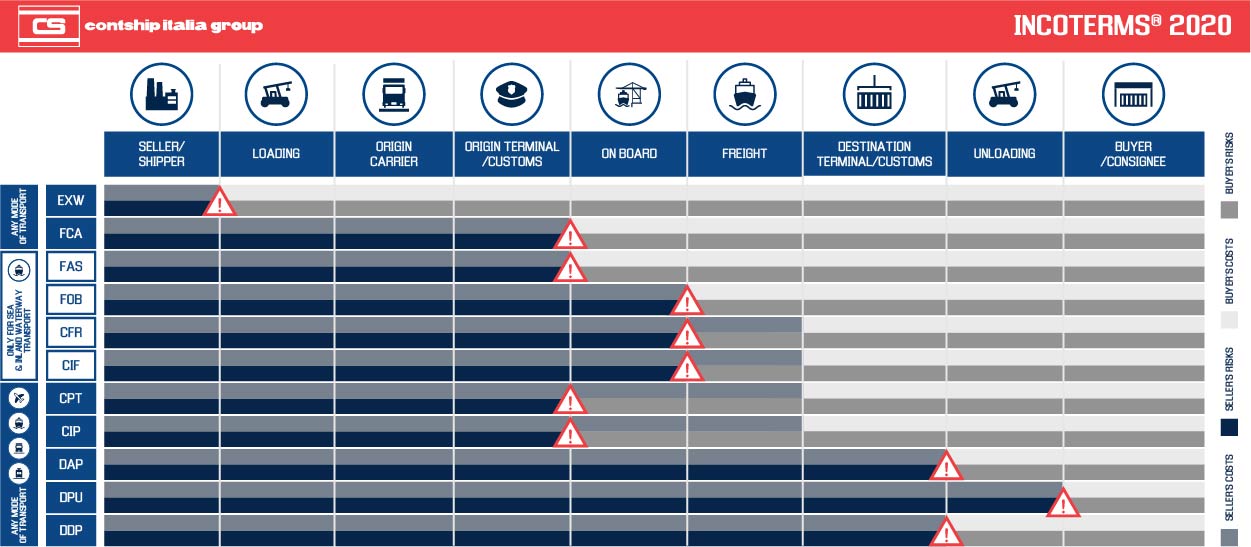

Incoterms® 2020 are 11 and can be classified according to their initial letter, which reflects the balance of the obligations borne by the seller and the buyer, or according to the mode of transport used.

Group E contains only the Ex Works term, which is the one with the greatest obligations for the buyer.

Group F contains 3 types of clauses (FCA - Free Carrier, FAS - Free Alongside Ship and FOB - Free On Board) in which the main freight is paid by the buyer.

Group C contains 4 types of terms (CPT - Carriage Paid To, CIP - Carriage And Insurance Paid To, CFR - Cost and Freight and CIF - Cost, Insurance and Freight), in which the transport is paid by the seller but the buyer takes the risks.

Finally, group D contains 3 types of clauses (DAP - Delivered At Place, DPU - Delivered at Place Unloaded and DDP - Delivered Duty Paid) in which transport and risks are borne by the seller.

By classifying the terms by mode of transport, we can distinguish between the Incoterms that can be used for any mode of transport (where we find EXW, FCA, CPT, CIP, DAP, DPU and DDP) and those applicable only in the case of sea and water transport (i.e. FOB, CFR and CIF).

Let's now go through the main characteristics of the individual Incoterms.

EXW - Ex Works

It is the term that involves the minimum level of obligations on the part of the seller and, conversely, the maximum level of risks and costs for the buyer.

In the term EXW, the seller is obliged to make the goods available to the buyer on their premises (generally the warehouse or its factory).

When the seller fulfills his obligation to make the goods available, the costs and risks of transport pass to the buyer, who will have to take care of the transport and customs clearance of the goods "from the seller's premises" to the final destination.

FCA – Free Carrier

With the FCA clause, the seller is obliged to deliver the goods to an agreed place and arrange for any export operations.

In the event that delivery takes place at the seller's premises, the risks and costs pass to the buyer when the goods are loaded on the carrier's means of transport made available by the buyer.

On the other hand, in the event that the delivery takes place at another agreed place, risks and costs pass to the buyer when the goods reach that place, but they have not yet been unloaded from the seller's means of transport and made available to the carrier appointed by the buyer. This means that if the delivery takes place outside the seller's premises, the latter is not responsible for unloading.

FAS - Free Alongside Ship

This term can only be used for maritime and inland waterway transport.

With the FAS clause, the seller fulfills the delivery obligation (with the related transfer of risks and costs) when he makes the goods available next to the ship chosen by the buyer in the agreed port of shipment. Added to this obligation is the burden of providing for any customs export operations.

The term FAS does not provide for customs clearance obligations for goods on import or for the stipulation of insurance contracts.

FOB – Free On Board

As for the FAS clause, this return can only be used for maritime and inland waterway transport.

With the term FOB, the transfer of risks and costs takes place when the seller places the goods on board the ship designated by the buyer in the agreed port of loading. Added to this obligation is the burden of providing for any customs export operations.

The term FOB does not provide for customs clearance obligations for goods on import or for the stipulation of insurance contracts.

Although the stipulation of the FOB clause implies that the costs for loading the goods on board the ship are to be borne by the buyer, in international commercial practice it often happens that these costs are borne by the seller. In such cases, the wording "stowed" is added to the abbreviation FOB, to specify that the seller bears, in addition to the costs of putting on board, also those for the stowage of the goods.

CFR – Cost and Freight

The obligation to deliver in the CFR term is fulfilled, as in the case of the FOB clause, when the seller places the goods, possibly cleared for export, on board the ship designated by the buyer at the agreed port of shipment, without the obligation to take out an insurance policy for transport from the port of loading to the port of destination. Unlike the term FOB, however, the seller is obliged to bear the costs of transport to the agreed port of destination.

This clause, like CPT - Carriage Paid To, CIP - Carriage And Insurance Paid To and CIF - Cost, Insurance and Freight returns, therefore presents a variance between the time of passing of costs and the time of transfer of risks.

Another critical element in the CFR term is the fact that the port of shipment, that is the one in which the transfer of risks to the buyer takes place, is not always specified in the purchase contract, unlike the port of destination, where the costs are passed on to the buyer. It is therefore in the buyer's interest to clearly specify both ports in the contract.

Finally, if the seller's transport contract includes the costs of unloading the goods at the place of destination, the latter cannot be recovered from the buyer, unless otherwise explicitly agreed in the sales contract.

CIF – Cost, Insurance and Freight

Last term that can be used exclusively for transport by water, the CIF clause has the same characteristics as the CFR term, with the only difference that the seller is also required to provide minimum insurance coverage for transport (Institute Cargo Clauses level - C or similar).

Also, in this clause, therefore, the delivery (and the passing of risks) takes place when the seller places the goods, possibly cleared for export, on board the ship designated by the buyer at the agreed port of loading.

Consequently, starting from the moment in which the goods have crossed the ship's side, the risks of loss or damage to the goods and any additional costs pass from the seller to the buyer.

On the other hand, the seller's obligation remains to bear the costs of transport to the agreed port of destination, again causing a difference between the time of transfer of risks and the time of passage of costs.

CPT – Carriage Paid To

In the CPT term, the seller is responsible for the transport of the goods to the agreed place of destination and the export customs clearance activities. However, the seller is not obliged to take out an insurance contract.

The delivery of the goods and the transfer of risk take place when the seller returns the goods to the carrier appointed by him. From that moment on, all risks of damage or loss of the goods pass to the buyer.

In the event that the transport involves the use of multiple carriers, as in the case of intermodal transport, the seller fulfills the delivery obligation when the goods are returned to the first carrier in the chain.

CIP – Carriage And Insurance Paid To

With the CIP clause, the seller has the same obligations under the CPT term, that is, he assumes the costs of transport to the place of destination and the export customs clearance activities. Unlike the term CPT, these obligations are supplemented by the burden of taking out insurance coverage against the risk of loss or damage to the goods during transport.

The insurance coverage must be of the Cargo Clause A type, thus guaranteeing maximum insurance coverage for risks, apart from those explicitly excluded.

The passage of risk therefore takes place once the seller has made the goods available at the place of delivery agreed with the buyer, which does not necessarily coincide with the final destination. For this reason, it is recommended to clearly specify both places of delivery and destination of the goods.

DAP – Delivered At Place

With the DAP return, the seller assumes the costs and risks related to the transport of the goods to the indicated destination, together with any export customs clearance operations.

The transfer of risks takes place when the seller makes the goods available to the buyer at the agreed destination, but before these are unloaded.

Import customs clearance formalities remain the responsibility of the buyer, who will also have to bear any risks and costs related to the storage of the goods waiting to be cleared through customs.

If the seller's transport contract includes the costs of unloading the goods at the place of destination, the latter cannot be recovered from the buyer, unless otherwise explicitly agreed in the sales contract.

DPU – Delivered at Place Unloaded

The term DPU is one of the novelties of Incoterms® 2020, as it replaces the previous DAT (Delivered at Terminal) by extending the concept of place of destination from the terminal (sea, airport, intermodal) to any place agreed between the parties.

With the DPU clause, the seller is obliged to make the goods available to the buyer, at the agreed destination, after having unloaded them from the means of transport and having completed any export formalities.

The seller assumes all risks and costs associated with the transport of the goods to the place of destination but is not obliged to enter into an insurance contract, nor to provide for any customs import operations.

DDP – Delivered Duty Paid

With the DDP clause, the seller assumes all the costs and risks already provided for in the DAP return, to which is added the obligation to clear the goods also for import, taking care of the import duty and taxes.

The seller therefore fulfills the delivery obligation when he makes the goods available, already cleared for export and import and ready for unloading, at the agreed destination.

For the use of this term, it is important to verify that the seller can directly or indirectly obtain the import license.

DDP term represents the opposite extreme compared to EXW. While in the first the maximum level of risks and costs lies with the seller, in the second it is the buyer who bears the maximum level of obligations.

Summarizing some fundamental points:

-

In all terms, except EXW, the seller is obliged to take care of any export customs clearance operations.

-

The DDP clause is the only one that provides for the seller the obligation to clear the goods also for import, taking charge of the import duty and taxes. In all other cases these obligations are the responsibility of the buyer.

-

In all terms, except EXW, the seller is required to load the goods on board the means of transport.

-

In all terms, except in the DPU, the buyer is obliged to unload the goods at the place of delivery.

-

In the terms CPT, CIP, CFR or CIF, the moment of passage of the risk from seller to buyer does not coincide with the moment of the passage of transport costs.

The level of complexity to be faced when choosing the term to apply to a sales contract, especially in the case of import-export, is undeniable. Unfortunately, too often risks and costs are underestimated, especially by the buyer, who tends not to be interested in logistics and transport processes, still perceiving them as a cost to be reduced rather than as an important element of the value chain.

Incoterms EXW and FCA: which term protects companies that deal with exports to third countries?

The EXW term in international transactions with non-EU markets is inadequate and risky from a customs and tax point of view.

The seller has the only obligation to make their goods available in the agreed place (factory, warehouse, etc.) as well as the delivery of commercial documentation.

In this type of clause, the burden of completing customs formalities rests on the buyer, with the risk that the latter does not promptly make a copy of the customs documentation to the seller / exporter, with the consequence that the latter may have difficulty justifying the correctness and the successful completion of the export customs operation, leading to potential risks of dispute and related administrative sanctions by the tax agencies responsible for controls.

With the FCA term the seller / exporter has the following obligations:

-

deliver the goods to the carrier appointed by the buyer or arrange for loading if the carrier arrives at its warehouses

-

deliver the commercial documentation for sending goods abroad

-

carry out, in its own name and care, the customs export operations

Using FCA all the risks of a customs and fiscal nature mentioned above can be avoided and, above all, it is possible to issue the transfer invoice "Non taxable art. 8, paragraph 1, letter A", which provides the exporting company with the following advantages:

-

certainty of carrying out the customs export formalities at the Customs Office responsible for the area

-

rapidity in verifying the actual exit of goods from the EU and / or remedying it through their competent customs, with any administrative closures

In light of the foregoing, it is desirable for exporting companies to think about whether or not to use the EXW term again.